Share prices avoid a severe battering from Covid-19

If you picked the right companies in the compound semiconductor industry, your shares will have

seen substantial gains over the last 12 months.

BY RICHARD STEVENSON

Although there is more than half the year still to go, there is no doubt what 2020 will be remembered for. Covid-19 continues to dominate the agenda, and is likely to do so for the foreseeable future.

One way to assess the devastation of this global pandemic is to consider its impact on the world’s health. The death toll is now north of 300,000, and is sure to finish far higher. But even that alarming number fails to capture the full extent of its destruction. A meaningful assessment must also include the ramifications of the reductions in treatment of other conditions, such as cancer; the consequences for mental health; and a shortening of life expectancy, resulting from a loss of earnings. Another aspect to consider is the economic fallout. Many millions have already lost their jobs, and it is not clear when some sectors will start to recruit again.

There are many ways to track the economy. There are employment figures, gross domestic products and yet another barometer that may be harder to interpret – the stock market. When Covid-19 transitioned from epidemic to pandemic in the early months of this year, shares fell at breakneck speed, but since then there has been significant recovery, probably reflecting that the situation could have been far worse. By the end of April the Dow Jones had fallen by less than 10 percent over the last twelve months, while the tech-heavy NASDAQ had climbed nearly 8 percent, an astonishing gain given the devastation caused by Covid-19.

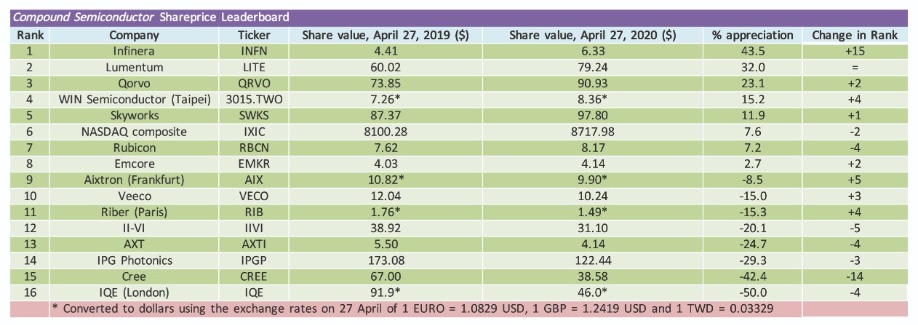

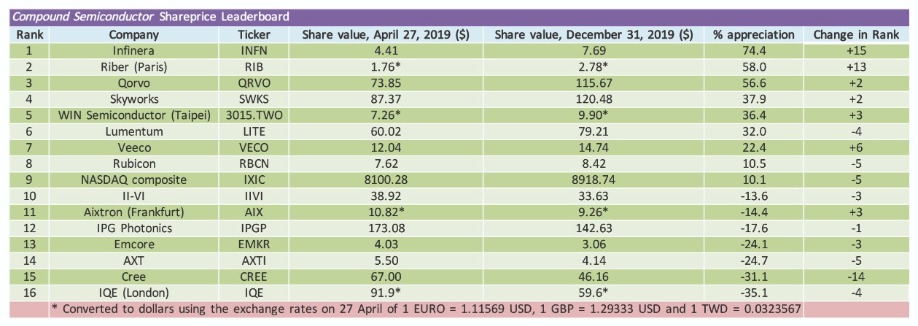

What about shares in the compound semiconductor industry? Well, throughout the latter part of last year many made significant gains – and in general, those that set the pace back then are still leading the pack, having undergone significant increases in valuation since April 2019. This is illustrated in the two Share Price Leaderboards produced for this year: one considers a year of trading up until 27 April, and the other evaluates the period between 27 April 2019 and New Year’s Eve, a timeframe where Covid-19 had no impact in any stock market.

In early April 2020 Infinera released its GX Series of compact modular solutions. This is claimed to add improved scalability and carrier-grade features to modern data centre-style networking approaches.

Riber’s rise and fallCompare them and you’ll see that Riber, the French manufacturer of MBE tools, is bucking the trend of most of the companies with significantly different standings in our two tables. Its share price shot up in late 2019, but has fallen steadily throughout this year to just below where it stood in Spring 2019, with declines beginning well before the pandemic spread to Europe.

It is likely that the soaring share price in November and December 2019 came from a flurry of significant equipment orders that have not continued into this year. In the last two months of 2019 Riber revealed several new orders, totalling six machines for research and one more for production. This promised to provided substantial growth in total sales, but it didn’t, due to a collapse in evaporator sales to makers of OLED-based products.

This substantial shift in the breakdown of Riber’s revenue is revealed in its results for fiscal 2019. For that year income from MBE systems contributed Ä23.0 million, up 140 percent year-over-year, while evaporator sales plummeted from Ä11.6 million to just Ä1.0 million. The third source of income, contracts for services and accessories, had a modest annual decline, falling from Ä10.1 million to just Ä9.4 million. The upshot of all these changes: revenue stood at Ä33.4 million, up Ä1.9 million over the previous year.

Riber has just reported its first quarter results for 2020. The order book is down 18 percent compared with the same time in 2019. There are no orders for evaporators, said to reflect a lack of investment within the OLED screen industry, while orders for systems are totalling Ä18.9 million and those for services and accessories ae worth Ä7.6 million. The reduction in the bookings has been caused by the pandemic, which has led to difficulties in finalising contracts with Asian customers.

Another consequence of the rise of Covid-19 infections during March and April has been a lockdown in France. Some of Riber’s employees are now working from home, while others are going to the site, enabling the company to still produce and deliver. Strategic projects are also running. However, Riber is facing a slowdown in commercial activity, with orders deferred, especially from China. Riber hopes this will not continue, given that China is its biggest market, where the 5G market is claimed to be “very buoyant”.

Infinera’s share price has shot up over the last twelve months, but is still below its value from April 2018.

From bottom to top

It’s been an encouraging 12 months for Infinera, the vertically integrated manufacturer of telecommunication equipment. This US-based firm has moved from last place on our Leaderboard to pole position, thanks to a share price that climbed from below $5 in late April 2019 to almost $8 by the end of the year and did not suffer from a substantial decline during the first few months of 2020. Note, however, that Infinera’s current valuation is still well short of the April 2018 price of almost $12.

The reasons behind both the rise in Infinera’s share price and the fall in its valuation over the last few years are illustrated in the company’s financial results. Take a look at the figures for the fourth fiscal quarter 2019, reported on 25 February 2020, and you’ll see that the profitability realised several years ago is either tiny or gone, depending on how you do the accounting, but gross margins and sales are heading in the right direction. Revenue for the fourth quarter exceeded guidance, hitting $384.6 million, which is up $59.3 million sequentially and a gain of $52.5 million compared with the equivalent quarter of 2018. Meanwhile, gross margin for the fourth quarter is 29 percent, up 2.3 percent sequentially and an increase of 3.6 percent year-on-year – but well short of the values north of 40 percent, reported around 2015.

During a call discussing fourth fiscal quarter earnings on 25 February, those leading the company painted a promising picture for the future. Reasons for an upbeat outlook included growing revenues, a diversified customer base and an expanded product portfolio.

According to company CEO Tom Fallen, fiscal 2020 will witness an important milestone in Infinera’s high-performance optics – it will mark a transition to fifth-generation, 800-gig capable technology that features digital signal processing (DSP).

Share price leaderboard 2020

“With fifth-generation technology creating significant performance and cost advantage for customers, we see a tremendous opportunity for Infinera to grow market share while also expanding our margin through our vertical manufacturing advantage,” said Fallon.In his opinion, vertical integration, which has historically provided a way to reduce cost, is now critical to success in the market place. And this is good news for Infinera, as it limits the number of competitors.

“We do not see commercial optical components being broadly available for 800-gig until late this year or 2021,” claimed Fallon. “By designing and manufacturing our own DSP and optical components, we expect to deliver 95 gigabaud fifth-generation optical systems to the market before commercial components are widely available.”

Another development that Fallon expects to aid Infinera is the prioritisation of 400-gig products by commercial DSP manufacturers. “This creates a scarcity in sources of supply for 800-gig technology and opens a tremendous opportunity for those that are vertically integrated and early to market.”

Infinera remains on track to deliver 800-gig product during the second half of this year, with revenues expected to ramp in 2021.

During the February earnings call, Infinera provided a financial outlook for the future. For the first fiscal quarter 2020 revenue is expected to be $315 million to $335 million. This figure included a $15 million impact from the coronavirus, due to ancillary merchant optics sourced from the Wuhan area.

Nancy Erba, Infinera’s CFO, also spoke in the call, providing an outlook beyond the third fiscal quarter. Back in February she said that the market that Infinera serves is expected to grow at around 6 percent – but it could be less than this, depending on the extent of the Covid-19 outbreak. She predicted that Infinera’s growth would outpace this, due to the positioning of its portfolio, with gross margin climbing by 2 to 4 percent in both fiscal 2020 and fiscal 2021. “Into 2022, we expect to continue growing faster than the market and achieve our target business model of gross margins in the mid-40 percent and double-digit operating profit,” said Erba.

Share price leaderboard for the time period up until the end of December 2019

When Erba updated investors in an earning call detailing the results for the first fiscal quarter 2020, she said that this long-term model remains intact, arguing that the drivers to achieve it are sound. However, due to the current market conditions, she explained that Infinera is now refraining from providing an outlook for the latter half of the year.The most recent quarter has not been a good one for the company. While revenue met guidance, with sales totalling $331 million, gross margins dived to 23.3 percent, 5 percent below expectations. This did not go down well with investors, as the share price plummeting by more than 10 percent.

One of the reasons behind the fall in gross margin is the involvement in a subsea consortium build, coming a quarter early. The other issue is related to substantial shipments of the company’s 200-gig Groove solution, which is based on merchant optical engines.

Fallon revealed during the call that during the quarter Infinera experienced supply chain disruptions, due to many countries imposing public health restrictions that impacted the production and delivery capabilities of the company’s vendors around the world. “This disruption had a negative impact on our ability to fulfil certain customer requests during the quarter.”

Looking ahead, Fallon is concerned that the macroeconomic uncertainty felt by Infinera’s customers could more than offset the continued expansion of bandwidth demand. “To address this uncertainty, we are taking proactive measures to reduce operating expenses and improve gross margin.” Measures that taken include a temporary reduction of salaries for senior management and the Board of Directors, and staffing reductions, largely in the area of contract positions – they are said to have little impact on the company’s regular global worker force.

These steps are expected to deliver savings of between $5 million and $7 million, and should have an impact on results for the second fiscal quarter. Guidance for that is revenue of between $310 million and $330 million, and a gross margin of 27 percent to 31 percent.

Qorvo claims that it is supporting Samsung’s Galaxy S20 platform with a broad set of high-performance, highly integrated components.

Lumentum’s climbUp one place from last year, Lumentum is now taking second spot on our Leaderboard, thanks to a share price that has risen from around $60 to $80 during the last twelve months.

The increase in the valuation of this manufacturer of many forms of laser reflects an improved balance sheet. For example, for the second fiscal quarter of 2020, ending on 28 December 2019, sales netted a record $457.8 million, up $7.9 million sequentially and $84.1 million year-over-year. Gross margins also improved over that timeframe, increasing from 33.4 percent for the second fiscal quarter of 2019 to 37.3 percent and 41.3 percent for first and second fiscal quarters of 2020, respectively.

On 5 May the company reported the results for the third fiscal quarter 2020. For that three-month period, ending on 28 March 2020, the Covid-19 pandemic had a significant impact on sales and margins. Quarterly sales dropped to $402.8 million – that’s $10 million below prior guidance given on 4 February that anticipated an impact from the pandemic of $15 million to $20 million. However, this shortfall did not alarm investors, nor the lower guidance for the fourth quarter, with the share price nudging up a few percent following the release.

During the call on 5 May, company CEO and founder Alan Lowe explained that the pandemic is expected to diminish fourth fiscal quarter revenue by more than $90 million: “Little more than half of this $90 million is a result of our inability to supply communication products, due to both component sourcing and production limitations – and the balance is from reduced consumer and industrial market demand.”

While the short-term impact of Covid-19 is not good for business, the changes it brings in the longer term could be, reasoned Lowe. “We believe Covid-19 will accelerate the shift to increasingly digital and virtual approaches to work, entertainment, education, health care, social interaction and commerce around the world.”

In autumn 2019 Lumentum moved its headquarters to a three-building office campus, known as Ridder Park Technology Center.

According to Lowe, those changes could lead to an increase in sales of high-performance optical devices, needed to address demand for higher capacity in communications and cloud networks. What’s more, sales of lasers for 3D sensing could rise, due to greater demand for the consumption, production and communication of digital and virtual content.Lowe provided a great deal of detail on the impact of the pandemic on the company’s various facilities.

At Lumentum’s factory in Shenzhen, China, many employees worked through the Chinese New Year holiday so that the company could quickly ramp production at the factory when the nation returned to work. But this plan has been hampered by difficulties in obtaining components from third-party suppliers inside and outside China. The situation is improving, but will have some impact on fourth-quarter results.

Lowe explained that at the Thailand facility, employee protective measures were rapidly implemented in the third quarter. “These measures had not limited output so far, but production in Thailand has been impacted by the same challenges that our Shenzhen factory is experiencing with sourcing components.”

In Malaysia, Lumentum has a contract manufacturing partner for most of its telecom transmission products. Due to local government action to address the pandemic, production halted for several weeks from mid-March, and has been slowly ramping since then.

Operation continues at Lumentum’s wafer fabs, located in the US, Japan and the UK. They are used to make datacom chips, telecom transport and commercial laser products, and telecom transmission products, respectively. At these sites, social distancing measures are a drag on efficiency.

Like many companies, staff that can work from home are doing so. “The increase in network traffic we have created with our virtual meetings, where we have added more than one million median minutes per week since early February, is an indicator of bandwidth growth,” said Lowe, citing this as further evidence that the future is very bright for Lumentum.

Before the Covid-19 outbreak, demand for Lumentum’s telecoms and datacom product lines was “very strong and accelerating”, according to Lowe, with volumes constrained by supply. Demand maintained its strength throughout the third quarter, but revenue fell 6 percent, with the pandemic exacerbating existing supply challenges. Despite these issues, Lumentum continues to grow its sales for voltage-controlled oscillators and InP high-bandwidth products for 600 gig and 800 gig systems.

Lowe revealed that quarter-on-quarter sales for the telecom transport product line were “approximately flat”, while datacom chip revenue climbed 20 percent sequentially.

Due to seasonal factors, Lumentum’s revenue from its industrial and consumer product lines fell by 24 percent compared with the previous quarter. However, sales were up 40 percent year-over-year.

In the third quarter, the company ramped production of its lasers for world-facing cameras and LiDAR for consumer applications. But now, due to Covid-19, sales of its lasers for 3D sensing are expected to drop by more than 40 percent, due to weak consumer demand and the potential for smartphone supply challenges.

A decline in fibre laser sales during the third quarter led to a $43.5 million fall in revenue. “We expect over the next several quarters, that our fibre lasers business will soften further, as it is tied to growth in global manufacturing,” said Lowe.

Despite the uncertain future, Lumentum is recruiting. At its facility in the UK, it hopes to add around 200 staff so that it can ramp its transmission products.

The company is giving to its community during the outbreak. “We have used our commercial supply chains to procure and donate personal protective equipment to health care providers,” said Lowe. In addition, Lumentum has expanded its charitable donation programmes, and its staff have been using internal capabilities to produce and donate limited quantities of PPE.

Qorvo: 5G growth

Another company that has seen a gain in valuation after releasing its latest quarterly results is Qorvo. It has taken third spot on this year’s Leaderboard, just outperforming peers WIN Semiconductor and Skyworks.

Qorvo’s balance sheet shows that it is going from strength to strength. For fourth fiscal quarter 2019, ending on 28 March 2020, sales netted $787.8 million, up $106.9 million year-over-year, while gross margins climbed by 3.4 percentage points to 42.6 percent.

Uptake of 5G is helping to swell sales. “Products like our 5G ultra-high-band solutions are being adopted across customers and on all leading 5G chipsets,” said company President and CEO Robert Bruggeworth during fourth quarter earnings call on 7 May. Some of these products, including what is described as mid-high-band and ultra-high-band 5G solutions, are going into Samsung’s Galaxy S20 platform.

Further sales related to 5G are coming from shipments of GaN high-power amplifiers and small-signal components supporting sub-6 gigahertz 5G networks. “Demand for Qorvo’s products has been robust, driven by the ramp of massive MIMO antennas,” says Bruggeworth.

The capabilities of Qorvo have grown this year through the acquisitions of Custom MMIC and Decawave. The former strengthens the portfolio of GaAs and GaN RF products for defense and aerospace, while the latter provides ultra-wide-band technologies for proximity awareness, secure payments, and secure access for smartphones, automotive and IoT.

Qorvo’s factories and engineering labs are remaining open during the pandemic. In addition, product development schedules are running, design and engineering teams are still developing new technologies, and the company is continuing to have strong interaction with its customers.

However, revenue will be down in the next quarter, due to the consequences of the Covid-19 outbreak. This is not impacting all product lines: while sales of mobile products are expected to fall, those from the infrastructure and defence division are expected to rise, thanks to greater demand for 5G infrastructure and the latest generation of Wi-Fi technology.

Based on all these considerations, revenue for the first fiscal quarter of 2020 should be between $710 million and $750 million. This range is wider than normal, reflecting greater uncertainty in the markets and the broader economy due to the effects of Covid-19.

IQE’s decline in income

Footing this year’s table is international epiwafer supplier IQE, which has seen its share price halve during the last 12 months. This fall reflects a decline in annual revenue from £156.3 million in 2018 to £140 million in 2019, resulting from reduced sales to a wireless customer that has been affected by changes in global markets and a photonics customer that has suffered from technical issues that are not related to IQE’s wafers.

Another key insight provided by the full year results, released on 28 April, is that despite the loss of a photonic customer, IQE’s revenue from this division increased by 4.4 percent to contribute £66.8 million, with half of those sales associated with VCSEL products. Meanwhile, wireless revenue fell by 22.4 percent to £68.2 million, due to a significant decline in volume from a GaAs power-amplifier customer. Loss in revenue has impacted the bottom line.

According to adjusted operating figures, IQE made a loss of $4.7 million last year, compared with a profit of £16 million in 2018. Company finances have not been helped by a bill for £4.3 million for legal costs, associated with a confidential patent dispute.

The Covid-19 pandemic is not having a major impact on production capability, with all sites around the globe remaining operational. As is the norm in the industry, staff are working from home where able. Other changes to operations include an increase in cleaning regimes and planning for shift segregation.

The outbreak has created much uncertainty in the market, and has led IQE to withdraw from offering specific guidance. However, it did reveal that its first-quarter trading exceeded expectations, and described the outlook for the second quarter as “positive”.

In the last few years, IQE has invested in infrastructure that should lead to higher margins and increased capacity. It has built a large foundry in Newport, South Wales, that has started to manufacture 3D sensing products; it has increased it wireless capacity in Taiwan to address changes in global supply chain dynamics; and it has built GaN capacity in Massachusetts to capitalise on forthcoming 5G infrastructure deployments. With all this in place, investment in property, plant and equipment is expected to significantly reduce in 2020 to below £10 million.

Despite the uncertainty in the near-term, IQE continues to invest in the generation of new products. It will spend £10 million this year developing: 10G and 25G distributed feedback lasers and avalanche photodiodes for high-speed datacoms and 5G fronthaul and backhaul; 5G switches and filters, which are based on its patented crystalline rare-earth oxide technology; long-wavelength VCSELs for future smartphone and LIDAR deployments; and lasers and sensors for environmental and health monitoring.

Such investment should serve IQE well. While the near-term may be tough, it has much promise for the future. It share price will surely rise, and like many companies from different sectors in our industry that have found themselves footing the table, it has the potential to rapidly climb up our Leaderboard.