GaAs RF Revenue to drop by 3.8 percent in 2020

Revenues impacted by dual influences of US-China Trade War and COVID-19 pandemic, says TrendForce

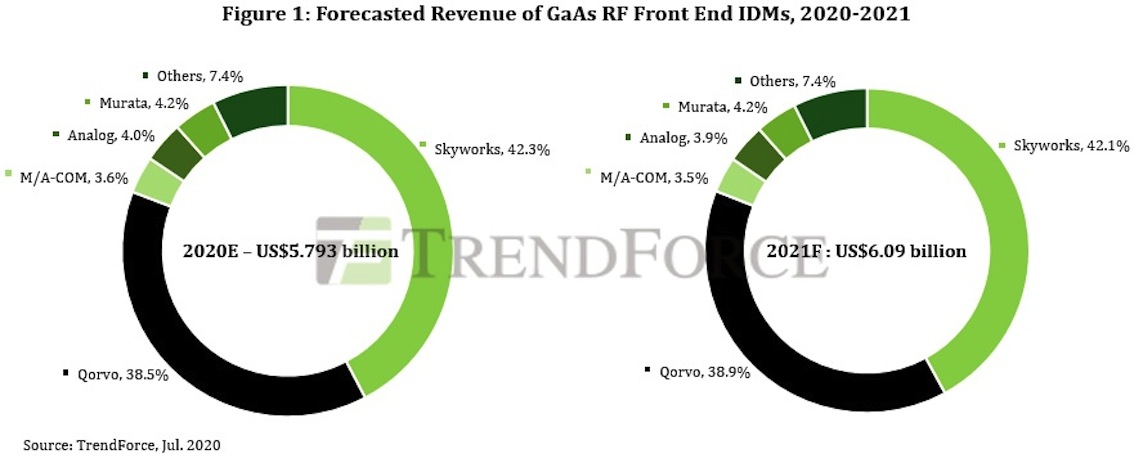

RF front-end component IDM and foundry revenues will be affected under the dual influences of the COVID-19 pandemic and the Chinese government’s policy of decoupling from the US, driven by the ever-intensifying US-China trade war that began in 2019, according to TrendForce’s latest investigations. Lowered demand for telecommunications end-devices in 2020 is also expected to lead to a bearish market for GaAs RF front end as well. GaAs RF front end revenue is projected to reach US$5.793 billion this year, a 3.8 percent decline YoY.

TrendForce analyst John Wang indicates that RF front end components can be classified according to their applications in various telecommunication devices. These applications include PA (power amplifiers), LNA (low noise amplifiers), and filters. Of the above applications, the GaAs compound semiconductor is particularly suited for use in PA components because of its high temperature resistance, high usable frequency range, and low noise under high frequencies. Furthermore, the number of PA components used in smartphones has increased along with the jump in cellular frequencies. For instance, 4G smartphones contain on average 5 to 7 PA parts per unit, while 5G smartphones contain 10 to 14 parts.

Despite continued impact from the US-China trade war, RF revenue is expected to recover in 2021 due to 5G development

Given the ever-intensifying US-China trade war, in which the US government increased tariffs on Chinese goods imported into the US, the Chinese government attempted to respond by instituting a policy of decoupling from the US and by importing goods and services from other countries instead. Nonetheless, China still depends on US-based IDMs for PA components and RF modules due to its insufficient R&D competencies for RF front end components. Although the trade war has lowered US IDMs’ revenues earned from Chinese clients, the fact that Chinese smartphone manufacturers must import some products from these IDMs means US IDMs were able to maintain their bottom lines to a certain extent. In 1Q20, Qorvo’s revenue grew by 15.7 percent YoY to reach $788 million, while Skyworks’ revenue decreased by 5.5 percent YoY to reach $766 million.

The overall GaAs foundry revenue was likewise disrupted by the US-China trade war in 1H19. In 2H19, however, under the influence of China’s decoupling from US goods and services, Chinese IC design companies decided to directly purchase from WIN Semiconductor Corp and AWSC. In 1Q20, WIN’s revenue grew by 67.8 percent YoY to reach $201 million, while AWSC’s revenue also increased by 162.6 percent to reach $27 million. On the other hand, GCS’ performance during the same period was relatively mediocre, registering a $12 million revenue, a 2.8 percent decrease YoY, in 1Q20, since operations at its primary fab, located in California, were affected by the pandemic.

TrendForce expects revenues of major RF front end IDMs to potentially make a rebound from rock bottom in 2021, as the global build-out of 5G base stations accelerates, and 5G handsets account for an increasing share of smartphone manufacturers’ yearly production. At the same time, some foundries are also likely to benefit from these circumstances, with the overall GaAs foundry revenue making an expected rebound as well.