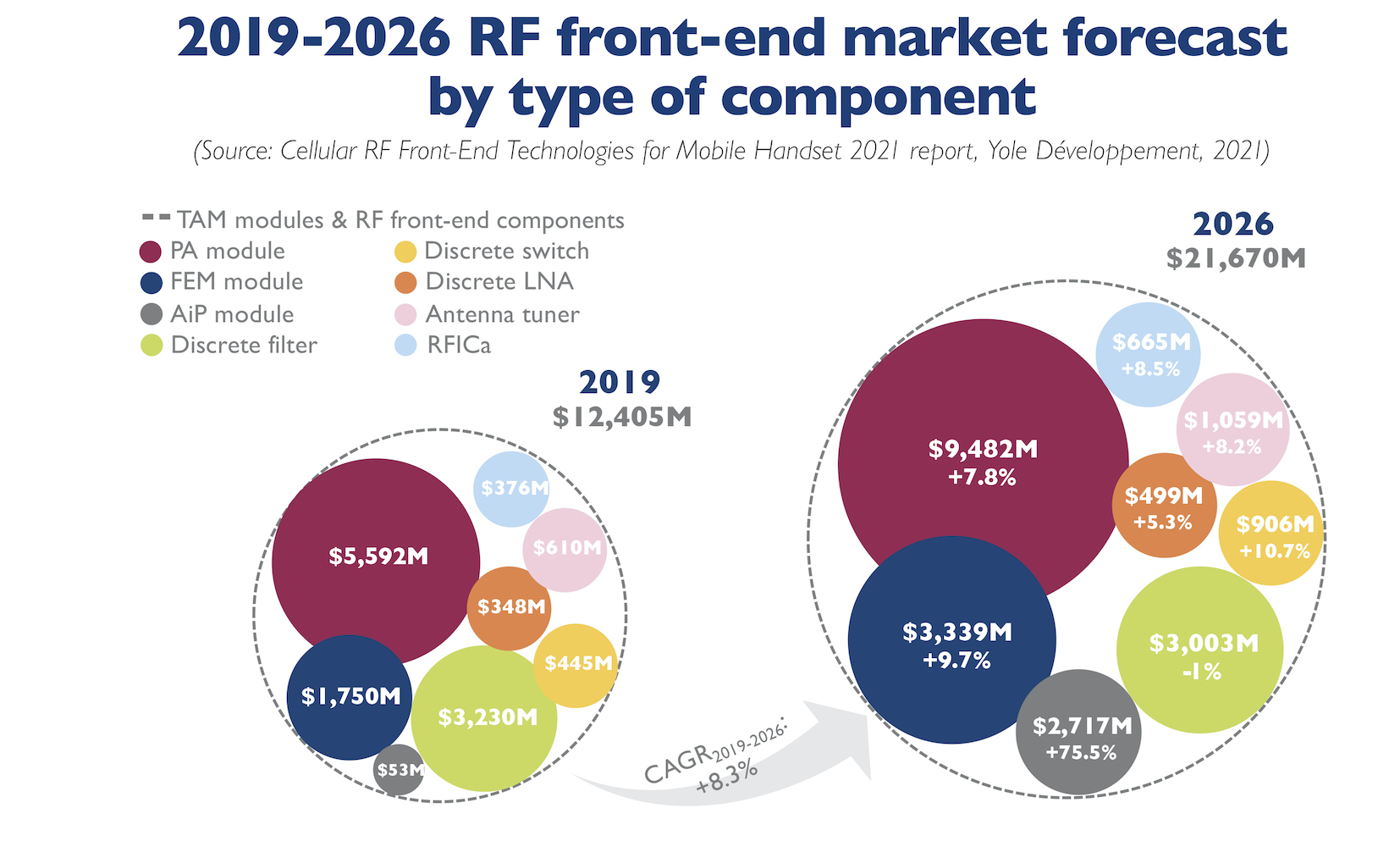

RF front-end market reaching $21 billion by 2026

The most attractive segment in 2026 will be the PA module with almost $10 billion, according to Yole Développement

According to Yole Développement's Cellular RF Front-End Technologies for Mobile Handset 2021 report, the number of 5G phones will more than double in 2021 compared to 2020, far faster than the LTE standard 10 years ago. And 5G is leading to an unprecedented increase in content of RF devices, while previous radio standards still need to be supported.

As a result, hundreds of RF components must be fitted into handheld format devices. This is now impacting mid-tier and entry-level phones, not only flagships. 5G features implemented in handsets focus on improving download speed and make the uplink more robust. In addition, there is an entirely new radio path created at mmWave frequencies, though this only applies to flagships right now.

A transition towards 5G

First use cases of the technology have matured and MNO are proposing new services to the consumer. MNOs are strongly motivated to invest more resources and to demonstrate 5G’s added value to the consumers, as 5G is not the first thing they are thinking about. In addition, MNOs have developed advantageous commercial 5G packages, particularly in China, adding some more motivation to consumers to upgrade.

In this context, 5G has strongly penetrated the smartphone market in 2020 and is expected to further grow as the network is expanding in China, in Europe and in the USA.

A 5G phone is relatively more complex than a 4G phone at the RF front-end level. And, as for every new air standard, 5G represents a significant opportunity for industry players to differentiate, innovate and win the market in the end.

As seen in the Cellular RF Front-End Technologies for Mobile Handset 2021 report, Yole’s RF’s team estimates the RF content as $5-$8 higher in a 5G phone compared to a 4G version and an additional $10 for a mmWave version.

As a result, the RF front-end market is booming. It should reach $17 billion by the end of 2021, up from $14 billion in calendar year 2020. From there, RF front-end market growth should slow. ASP erosion will be stronger when 5G is mainstream and competition grows further. Overall, analysts expect an 8.3 percent CAGR between 2019, the year of 5G’s introduction, and 2026, leading to a $21 billion RF front-end market.

The introduction of 5G adds complexity to phones along with RF content. Building 5G phones using discrete components while keeping an acceptable form factor is a challenge, driving more integration.

“The RF front-end market leaders all have flexible module offerings adapting to multiple market requirements. Besides that, some also have custom-built modules for the flagships” affirms Mohammed Tmimi, RF Technologies and related markets analyst at Yole. “As a result, Skyworks, Murata, Qualcomm, Qorvo and Broadcom together share 85 percent of the RF front-end market. Skyworks is the market leader”.

Qualcomm has the strongest growth. According to Stéphane Elisabeth, senior technology and cost analyst at System Plus Consulting: “At the end of 2019, Qualcomm had a smaller market share than the others supplier. This change in 2020, with OEMs like Samsung. The share of Qualcomm almost double at the beginning of the year. Yet, the situation changes at the end of 2019 with the release of the Apple phones. Indeed, the iPhone series doesn’t integrate a lot of Qualcomm’s component in its design. The goal of Apple is to avoid the use of Qualcomm completely in the future.”

However, a variety of companies coming from China are emerging and experiencing double digit growth in the RF front-end space. Most started in the discrete business with standalone LNAs or switches, which enabled them to accumulate know-how and establish trust with OEMs.

The next step for these fabless Chinese companies is to bring integrated modules to the market. This has been supported by more investments in China over the past two years. It’s likely that not all will succeed, but we can expect more cooperation and consolidation over the next few years.

A major difficulty for success will be the access to wafer capacity. There is not a shortage of RF components per se, more like tightness in the industry. This is pushing long term supply agreements that only big players can afford.