Mixed picture as TV shipments hit a post-pandemic high

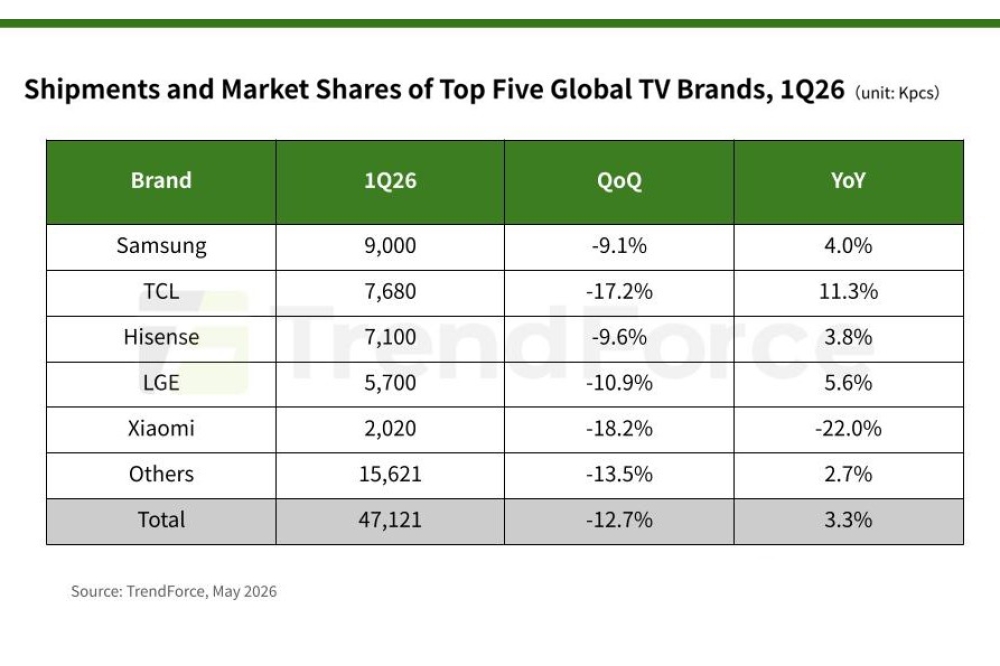

According to the latest research by TrendForce, branded TV shipments worldwide reached 47.12 million units in 1Q26, marking a 3.3 percent YoY increase and achieving a post-COVID-19 pandemic high for the same period. However, it's a mixed picture with a QoQ comparison showing a 12.7 percent decline.

TrendForce says that although the demand side of the TV market remained conservative in 1Q26 due to the traditional slow season and a reduction in China’s trade-in subsidies, the tight supply of DRAM and NAND Flash — driven by AI server and advanced computing demands — caused a significant price surge for memory components used in TVs in late 2025. To mitigate subsequent cost pressures, TV brands initiated early stocking activities and order pull-ins, which became the primary driver supporting shipment growth in 1Q26.

TrendForce states that with the continuous rise in the costs of memory and other components, the divergence in brands’ product strategies will become more pronounced in 2026. Top-tier brands that can leverage their scale and cost advantages will continue to promote high-end, large-sized, and Mini LED models. Other brands will gradually transition their main offerings from small-sized models to medium-to-large-sized models that adopt FHD resolution to alleviate cost pressures.

As brands adjust their shipment mixes with respect to product specifications and size, global TV shipments for 2026 are projected to register a slight 1 percent YoY decline to a total of 194.2 million units. This shipment decline in the TV market is significantly smaller than that of consumer electronics with memory representing a higher proportion of the overall device cost (e.g., smartphones and NBs).

Regarding the shipment performances of individual brands in 1Q26, the top five were Samsung, TCL, Hisense, LGE, and Xiaomi, in that order. TCL benefited from its expansion in North America and emerging markets, as well as its promotion of Mini LED and large-sized products. Its shipments reached 7.68 million units with an 11.3 percent YoY increase, the highest growth rate among the top five. TCL continues to narrow the gap with Samsung.

Xiaomi’s 1Q26 shipments fell by 22 percent YoY, impacted by the waning effects of China’s subsidy program and a strategic shift toward more profitable large-sized and mid-to-high-end models. Furthermore, surging memory prices drove up the production costs of its small- and medium-sized TVs, which further hampered its export performance.

Conversely, Skyworth has seen its shipment volume steadily expand in recent years after taking over Philips’ North American TV operations and securing brand licensing for Panasonic’s TVs. As a result of this continued growth, Skyworth has the potential to enter the group of top five in the global brand rankings for 2026.

Rising Memory Costs

TrendForce points out that surging memory prices have significantly increased cost pressures on small- and medium-sized TVs. In response, brands are accelerating the phase-out of low-margin products and shifting their focus to medium- and large-sized models. Taking 32 inch TVs as an example, the proportion of memory in the overall unit production cost grew from 6-7 percent to 15 percent in the first quarter. Consequently, shipments for this size category are projected to drop by 9.1 percent YoY in 2026, shrinking its share of this year’s global shipments to 19 percent.

Some brands that previously focused on small- and medium-sized TVs are also shifting toward entry-level, medium- and large-sized FHD models to help absorb the pressure of rising memory costs. In comparison, for 65 inch TVs, memory’s share of the overall unit production cost only rose from 2-3 percent to 10 percent in the first quarter. Hence, 65 inch and 75 inch will be the sizes primarily promoted by brands this year. Products 65 inch and above are estimated to account for nearly 25 percent of this year’s global shipments.

Beyond the trend toward larger screen sizes, Mini LED TVs have also emerged as a crucial segment for brands aiming to enhance product value and profitability this year. TrendForce projects that global Mini LED TV shipments will reach 24.9 million units in 2026, reflecting an 87 percent YoY increase. Driven by this robust growth, the market penetration rate of Mini LED TVs is expected to surpass 10 percent for the first time, reaching 12.8 percent.

Chinese brands are spearheading the mainstream adoption of Mini LED products through supply chain integration and cost reductions. The three major Chinese brands—TCL, Hisense, and Xiaomi — now hold a combined market share of 54 percent for Mini LED TVs.

Meanwhile, Samsung introduced an entry-level Mini LED lineup this year to offset profitability pressures stemming from rising memory costs. This strategic move is expected to boost Samsung’s market share for Mini LED TVs back to 30 percent, thus allowing the company to reclaim its top position in this segment. As product offerings continue to broaden, Mini LED technology is steadily expanding from high-end models down into mid-range segments.