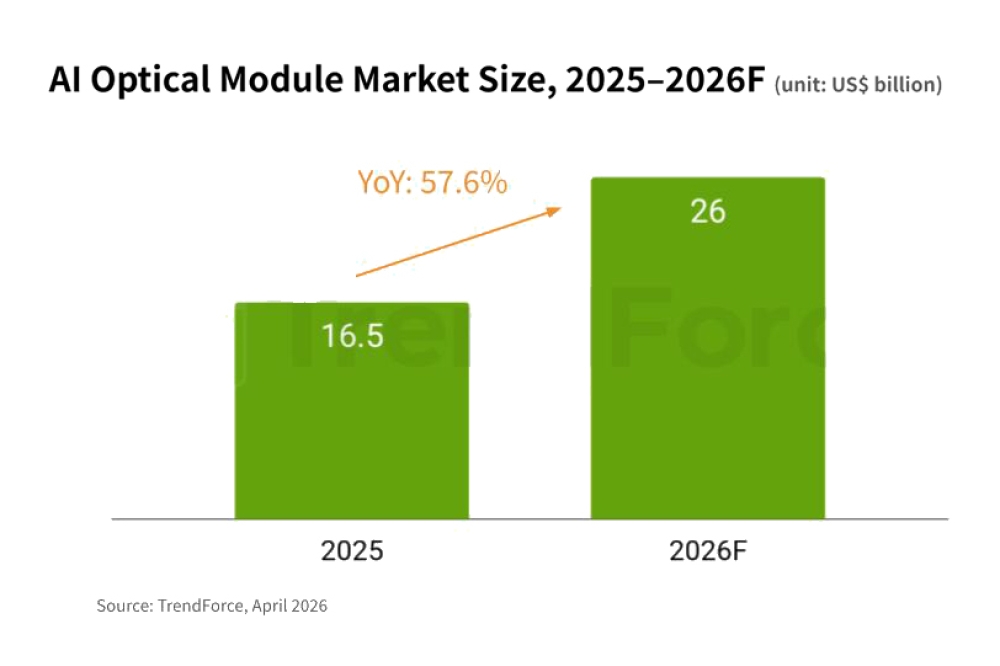

AI optical transceiver market to reach $26b in 2026

TrendForce’s latest research indicates that the global market for AI-focused optical transceivers has entered a phase of rapid growth, with market size projected to expand from $16.5b in 2025 to $26b in 2026, representing over 57 percent YoY growth.

This surge is driven not only by specification upgrades but also reflects a broader structural reshaping of the optical communications supply chain amid accelerating AI data center deployment.

Demand is rising sharply for 800G and above optical transceivers used in AI server cluster interconnects as AI data centers continue to scale. Traffic at hyperscale data centers in North America has sustained over 30 percent annual growth, prompting cloud giants such as Google, Microsoft, and Meta to expand GPU and AI server deployments. This has further boosted procurement of high-speed optical interconnects. Meanwhile, supply-side pressures are becoming increasingly evident.

TrendForce notes several key bottlenecks constraining capacity expansion. First, the supply of critical optoelectronic chips, such as electro-absorption modulated lasers (EMLs) and continuous-wave lasers (CW-LDSs), remains tight due to capacity allocation constraints.

Additionally, high-precision manufacturing processes, including optical alignment, limit scalable production. Power consumption and thermal management challenges also continue to affect system design and deployment timelines.

Upstream suppliers, led by NVIDIA and major system vendors, are mitigating supply risks by shifting procurement strategies and adopting strategic long-term agreements (LTAs) to secure key components and reduce reliance on spot-market purchasing. Meanwhile, technology roadmaps are accelerating toward low-power linear pluggable optics (LPO) and silicon photonics integration, aiming to replace traditional high-power DSP-based architectures and alleviate power and thermal constraints.

TrendForce further observes that growth in the AI optical transceiver market is shifting from single-product upgrades to three parallel drivers: market expansion, generational technology transitions, and application diversification. As the 1.6T generation gradually enters mass production, demand for edge computing and data center interconnect (DCI) will also drive expansion of the 800G and 1.6T ZR/ZR+ coherent optical module markets.

In response to tightening component supply, leading international players such as Coherent, Lumentum, and Applied Optoelectronics, along with Taiwanese firms such as Elite Advanced Laser Corporation (ELASER) and LuxNet Corporation, have initiated capacity expansions and technology deployments.

The upgrade cycle offers significant structural growth opportunities for Taiwan’s optical communications supply chain. Taiwanese firms have established solid capabilities in foundry services, EML laser chips, passive optical components, and module packaging and testing, with ongoing advancements in silicon photonics and LPO technologies. The years 2026 to 2027 are crucial for establishing a foothold in the 1.6T supply chain, where success in design-in at tier-one customers will likely be a key factor in determining future market share.