The growth of wide bandgap power devices

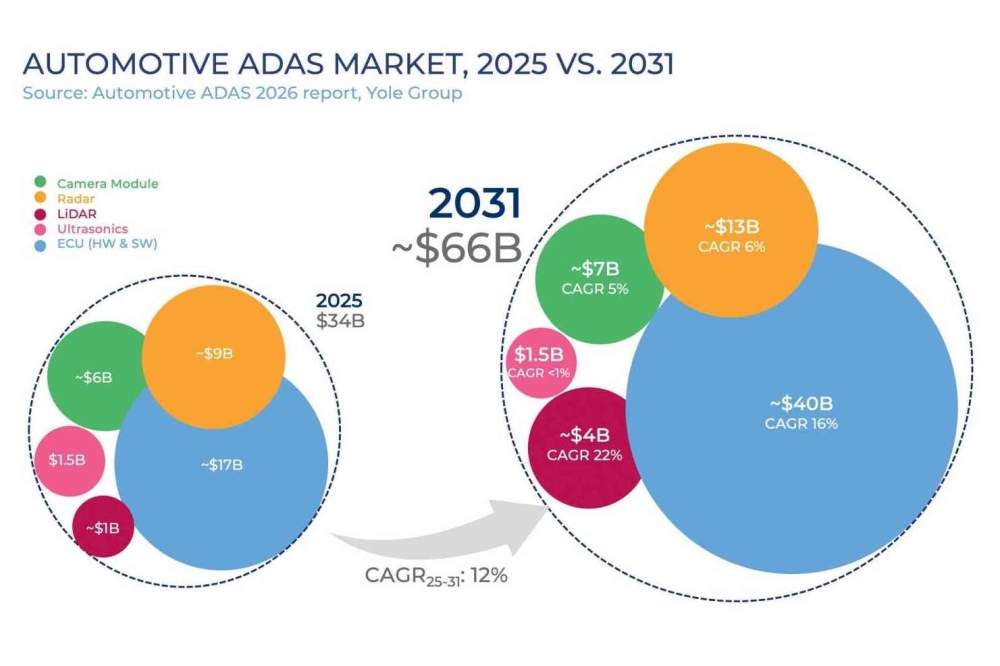

Surging sales of SiC and GaN devices, particularly within the automotive industry, are going to create a $10 billion market by the end of this decade.

BY POSHUN CHIU AND EZGI DOGMUS FROM YOLE GROUP

Supported by subsidies and motivated by cutting carbon footprints, more and more drivers are switching to electric vehicles. It’s a move that has implications that include helping to drive up revenue for wide bandgap technologies, today the combination of SiC and GaN. Collectively, these devices are expected to double their share of the semiconductor power device market over the next five years, according to our research at Yole Group.

We are now seeing sales of wide bandgap devices climb at great pace, more than 20 years after the first power SiC devices were commercialised. The rapid expansion of this market shows no sign of abating, with GaN technology poised to take off and assist in driving innovation in this segment.

Today, wide bandgap technologies accounts for more than 16 percent of the global power device market, and we forecast that this will jump to more than 32 percent by 2029.

Globally, more than $30 billion of investment has announced for SiC, with the focus on device manufacturing. Source: Power SiC – Markets and Applications 2024 report, Yole Intelligence.

By then, our expectation is that SiC device revenue will represent more than 26 percent of the semiconductor power market, with sales climbing to nearly $10 billion. To get there, revenue will increase with a compound annual growth rate of 24 percent from 2029, from a starting point of $2.7 billion in 2023. Over that timeframe, GaN revenue will grow from $260 million to $2 billion at a compound annual growth rate of 41 percent. Beyond then, we anticipate further growth, spurred by additional high-power and industrial applications.

One impact of two decades of development of wide bandgap technology is that it has led to almost every major player in the power semiconductor market having some business in SiC, and preparng for GaN business in the years to come. For the latter, revenue primarily comes from discretes, and system-in-package and system-on-chip products.

The long-term evolution of SiC is towards electric vehicles with 800 V

power trains and a number of industrial applications. Source: Power SiC – Markets and Applications 2024 report, Yole Intelligence.

Major players in the power electronics market with a sizeable SiC businesses include Infineon, onsemi and ST Microelectronics. Since 2017, the latter has been leading the way in SiC, after it took pole position by entering the supply chain of Tesla – a SiC pioneer in the automotive industry. Other significant manufacturers of SiC devices include Rohm, Bosch, Wolfspeed and Mitsubishi Electric.

SiC takes hold in automotive

A major milestone in the SiC industry came in 2001, when Infineon launched the first SiC Schottky barrier diode. It is a device that took many years to establish itself, and when emerging on a commercial scale 10 years ago, was a new innovation waiting for a market. These diodes, joined by MOSFETs from 2010 onwards, won deployment in industrial applications, such as power supplies and solar photovoltaic inverters. However, revenues only started to rocket when automotive original equipment manufacturers started adopting SiC power devices for 400 V battery EVs.

We have been tracking the SiC market for several decades, and predicted the rise in its value from around $100 million in 2013 to approaching $800 million in 2020.

The key partnership between STMicro and Tesla led to SiC first being deployed in the Tesla Model 3, in 2017. The EV maker then adopted SiC in its Model Y, before sales of these electric vehicles took off, and the SiC power device market started to grow rapidly. High volumes of SiC have been shipped to Tesla, but up until now they have only been incorporated in a relatively small number of models.

Where Tesla has led, others have followed, with several other OEMs incorporating SiC in their 400 V battery EV architectures. The next generation of EVs will be based on an 800 V battery system, a migration that will lead to more models featuring SiC technology and increasing its demand. And in parallel, we’ve seen generations of SiC MOSFETs being launched by different players, in order to provide the advantages of power conversion efficiency or high power-density in various applications.

This anticipated trend is contributing to substantial global investment in SiC, totalling more than $30 billion. In North America Bosch is investing $1.5 billion in a facility in Roseville, California, to expand its capacity, Wolfspeed is spending $3.5 billion, Coherent is investing $1 billion, and X-FAB is spending $200 million in Lubbock, Texas. Meanwhile, in Europe, ST Microelectronics is building a new €5 billion facility in Catania, Italy, next to its existing facility, onsemi is investing in epiwafer capacity in the Czech Republic, Nexperia is investing $200 million in Germany, and Vishay has acquired capacity in the UK.

Market forecasts for Power SiC and Power GaN in 2023 and 2029. Sources: Power SiC – Markets and Applications 2024 report, Power GaN 2024 report, Yole Intelligence.

These investments in North America and Europe, each total around $6 billion. It is a substantial sum, but still overshadowed by investment in Asia. In this region – where manufacturing is shifting to – spending is expected to total $8 billion in China alone, and more than $10 billion across the rest of Asia, including Japan, Korea, and Southeast Asia.

Within China, market leaders such as UNT, Sanan IC, YASC and HestiaPower have announced multiple investments.

What does all this investment mean for the market?

Our expectation is that while SiC revenue will grow in the next few years, up until 2026 these sales will be smaller than the planned total investment by companies in this technology. Due to this, SiC chipmakers will have to carefully control their injections into CapEx, so that they grow revenues on top of building new facilities. There will be some challenges, such as managing cash flow. One headwind to such activities is the slowdown in the EV market, driving the need for more sustainable investments to continue CapEx injection.

During these years of investment, the SiC industry is transitioning from 6-inch to 8-inch wafers. While chipmakers benefit from this migration, undertaking this upgrade to their infrastructure requires substantial financial resources. If they can weather this period, sunnier times will lie ahead, with declining spending and increasing revenue creating a more sustainable business.

The long-term opportunity for SiC is not limited to an increase in demand that stems from the roll-out of 800 V EVs. The increase in supply of SiC power devices, resulting from new capacity coming to market, will also enable more use of this technology in other applications, such as: high-power EV chargers; solar PV; and industrial applications, including motor drives, railways and wind turbines.

Another consequence of this multi-billion-dollar global investment in SiC is that the shortages in material supply and device capacity that occurred in 2019 to 2022 – when the majority of demand was secured by automotive customers, limiting penetration in industrial applications – will not be repeated in the coming years.

Considering GaN adoption, with a focus on automotive powertrain applications. Source: Power GaN 2024 report, Yole Intelligence.

GaN: A technology for tomorrow

In contrast to SiC, GaN emerged as a technology for consumer devices rather than automotive applications. The first devices were launched in 2010, creating a small market for fast smartphone chargers. Markets for consumer applications started taking off around 2018-2019, climbing to $260 million by 2023.

To ensure that GaN becomes another multi-billion market, suppliers are now looking to enter higher-value markets beyond sub-2kW consumer applications. These new opportunities include high-power automotive and industrial applications.

Manufacturers that are ramping up their GaN development and production include: Infineon, through its acquisition of GaN Systems; Renesas, which acquired Transphorm; Innoscience; STMicro; Texas Instruments; Navitas; and Nexperia.

There are a number of automotive OEMs and Tier 1 manufacturers interested in next-generation GaN technology. They include Hofer ZF and Ricardo, looking at GaN for inverters; UAES, Marelli and Inovance, developers of on-board chargers; and Vitesco and Valeo, considering GaN while pursuing DC-DC converters.

We expect it will take time for the automotive sector to adopt GaN. Used in consumer products today, GaN is generally viewed as a technology for tomorrow in the automotive sector.

The main GaN application is expected to be on-board chargers for battery EVs and plug-in hybrid vehicles with power levels less than 11 kW. The added value that comes from switching from silicon to GaN DC-DC converters does not justify significant adoption, especially at power levels less than 3 kW.

For main inverters with 400 V systems, GaN will not find it easy to enjoy commercial success. SiC and silicon are already well-established, and GaN power modules allowing operation at power levels above 50 kW are not yet available. For 800 V systems, 1,200 V GaN devices are not yet commercially available, while 650 V GaN has the potential to enter the inverter market with multi-level power topologies. Based on all of this, we are not expecting GaN adoption in main inverters to begin before 2029.

Another reason behind this view is that GaN technology is still relatively young. It takes time to validate reliability and refine the design. Today, major automotive or industrial OEMs are still developing GaN to implement in their vehicles. Motivation for this comes from the unique added value provided by GaN, which includes its higher efficiency than silicon and SiC. At this stage, GaN is tending to win deployment in the lower power range, while adoption in higher-power applications is being developed.

Over the last year or so, the view on what will be the next big application after the consumer market has shifted. Due to the emergence of artificial intelligence (AI) as the ‘next big thing’, there is much interest in using GaN to increase efficiency in the booming AI data-centre market. Each graphics processing unit consumes 1 kW, matching the power level GaN can provide.

There are different stages in the power supply for servers. There are power supply units (PSUs) in the 400 V AC-DC stages, DC-DC stages, and at the next level, to a lower voltage with a 48 V rating.

GaN is a technology suitable for all these requirements. As well as two major voltage ratings, 650 V and 400 V, which can support the PSU, it has a lower 200 V rating, which can match the 48 DC bus requirement that AI data centres demand today.

One of the biggest benefits of GaN is its ability to provide high efficiency, which will increase data-centre profitability by reducing running costs, helping comply with new regulations and trimming the carbon footprint. As the technology is ready, the key question is this: When will some of the big system players decide to take high volumes of GaN?

Device suppliers are striving to convince them that there’s cost parity with silicon devices, to be realised while enjoying higher efficiencies that deliver performance benefits.

We forecast that data centres will become one of the most important markets for GaN to enter. Once it’s adopted, growth will be strong, spurred by significant demand from AI. This could initially drive the market to nearly $2 billion, our forecast for 2029. Over the longer term, we see potential for GaN to enter industrial applications, as well as the automotive sector. However, consumer applications will still play an important role.

Today’s manufacture of GaN devices tends to involve silicon or sapphire substrates. However, alternative foundations are being proposed, and in some cases launched, such as Qromis Substrate Technology – a composite material substrate developed by US-based Qromis. This engineered platform suppresses cracking of the GaN epitaxial layer, enabling large-diameter epitaxial growth. In future, GaN chipmakers may also be able to turn to growth on silicon-on-insulator substrates.

From the technology perspective, we are seeing a lot of options for GaN uptake, as well as a lot of potential for GaN to enter different markets.

Over the coming years, GaN devices will win deployment in an increasing number of applications. Source: Power GaN 2024 report, Yole Intelligence.

Wide bandgap takes on key role

What’s clear is to all is that wide bandgap materials are playing a growing role in the semiconductor power electronics industry. This market is already worth several billion dollars, and has the potential for strong growth throughout the remainder of this decade and beyond.

After 10-to-20 years of development, SiC technology is now on the path to high-volume production and expansion. GaN technology will follow, but is still evolving and discovering different possibilities for future markets.